“This is the most attractive time to be acquiring residential loans since I started in the market in 1991,” said Carl Bell, a senior managing director at Invictus Capital Partners.

The amount of servicing outstanding in Ginnie MBS increased by 1.6% during the first quarter. Lakeview/Bayview Loan Servicing increased its market share thanks to large purchases of MSRs.

Issuance of MBS backed by expanded-credit mortgages increased by nearly 50% from the fourth quarter to the first quarter of 2024. Annaly more than tripled its volume.

All three agencies saw increases in monthly loan deliveries in April, with loan mods helping to boost Fannie to a 17.4% gain from March. The purchase market and cash-out refi remain strong. (Includes two data tables.)

Servicing outstanding increased by an estimated 0.3% in the first quarter. Meanwhile, Mr. Cooper Group, which recently became the largest primary servicer, boosted its portfolio by 14.6% from the end of 2023. (Includes three data tables.)

Complaints filed with the CFPB regarding mortgage servicing went up in the first quarter of 2024, while issues tied to mortgage originations declined. (Includes two data tables.)

Originations of purchase mortgages with primary MI coverage fell slightly in the first quarter, but the spike in refi activity, especially in the government market, more than made up the difference. (Includes four data tables.)

The guidelines lay out the process lenders must develop for borrowers to request an appraisal reassessment when they believe a valuation was inaccurate or biased.

Big increases in securitization of office-property and industrial mortgages lifted non-agency CMBS issuance to $21.9 billion in the first quarter, a 68.6% increase from the prior period. (Includes two data tables.)

Rocket’s originations and secondary market sales of home equity loans are flourishing without the GSEs. It’s also not yet clear how large of a role the GSEs would have in the market for closed-end second liens.

With Freddie finally increasing its STACR issuance in the first quarter, the GSEs’ slump in CRT activity could be abating. Older deals continue to be retired in a steady stream of tender offers by the enterprises. (Includes data table.)

Non-agency MBS issuance more than doubled on a sequential basis in the first quarter of 2024, with jumbo mortgages making up the majority of loans in the deals. (Includes three data tables.)

Originations of higher-priced loans, a proxy for subprime mortgages, declined in 2023 but held up better than total originations. (Includes two data tables.)

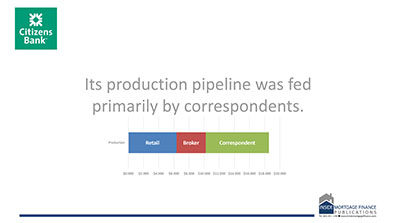

Agency securitizations of correspondent loans were sharply down in the first quarter of 2024 as volume dropped across the board. Refinances made a surprising surge, while credit quality remained unchanged. (Includes two data tables.)

Publicly traded banks reported a 21% increase in mortgage-banking income during the first quarter of 2024. Improving gain-on-sale margins accounted for much of the increase. (Includes data table.)

While overall correspondent sales to unaffiliated non-agency buyers declined in 2023, Veterans United increased its sales volume. (Includes data table.)

Philadelphia-based Republic Bank focused its mortgage production on jumbos with below-market rates. The bank also held agency MBS that lost value as interest rates increased.

The flow of refinance loans into the Ginnie MBS program dropped 9.2% in April. Still, year-to-date refi volume in the government-insured market was up a solid 54.4%. (Includes two data tables.)

A lender’s reconsideration of valuation process must include disclosure to the borrower at the point of a loan application and again when the borrower receives the appraisal.

Correspondent sales of government-insured mortgages originated during 2023 declined somewhat on an annual basis, but Veterans United upped its sales by 7.3%. (Includes data table.)

The Biden administration’s fiscal year 2025 budget request allocates $72.6 billion for HUD, which is higher by about $500 million from the FY23 enacted level.

Agency securitizations of correspondent loans were sharply down in the first quarter of 2024 as volume dropped across the board. Refinances made a surprising surge, while credit quality remained unchanged. (Includes two data tables.)

Originations of purchase mortgages with primary MI coverage fell slightly in the first quarter, but the spike in refi activity, especially in the government market, more than made up the difference. (Includes four data tables.)

Non-agency MBS issuance more than doubled on a sequential basis in the first quarter of 2024, with jumbo mortgages making up the majority of loans in the deals. (Includes three data tables.)

Big increases in securitization of office-property and industrial mortgages lifted non-agency CMBS issuance to $21.9 billion in the first quarter, a 68.6% increase from the prior period. (Includes two data tables.)

Mortgage deliveries to the mortgage-backed securities platforms of Fannie Mae and Freddie Mac rose in April, but credit trends suggest these were seasonal increases rather than a start of a new trend. (Includes two data tables.)

The flow of refinance loans into the Ginnie MBS program dropped 9.2% in April. Still, year-to-date refi volume in the government-insured market was up a solid 54.4%. (Includes two data tables.)

Mortgage deliveries to the mortgage-backed securities platforms of Fannie Mae and Freddie Mac rose in April, but credit trends suggest these were seasonal increases rather than a start of a new trend. (Includes two data tables.)

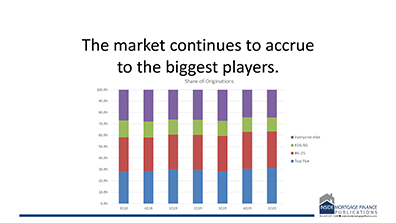

Even though Fannie Mae and Freddie Mac maintained healthy profits in a tough market in the first quarter, their capital shortfalls under the ERCF remained absurdly high. (Includes data table.)